Understanding the Basics of homeowners insurance is essential when buying a home, and protecting it with the right coverage is equally important. Many homeowners feel overwhelmed by the process, especially when faced with numerous options and unfamiliar terms. Insurance can seem complicated at first, but learning the basics helps you make smarter decisions. A little preparation can save you time, money, and stress in the long run. Knowing what to look for before you purchase a policy provides valuable peace of mind. By understanding the key aspects of home insurance, you can confidently select the best coverage for your needs. Every homeowner deserves to feel secure, so it's worth taking the time to get it right. Now, let's explore the essential things every homeowner should know before buying insurance.

Understanding the Basics of Homeowners Insurance

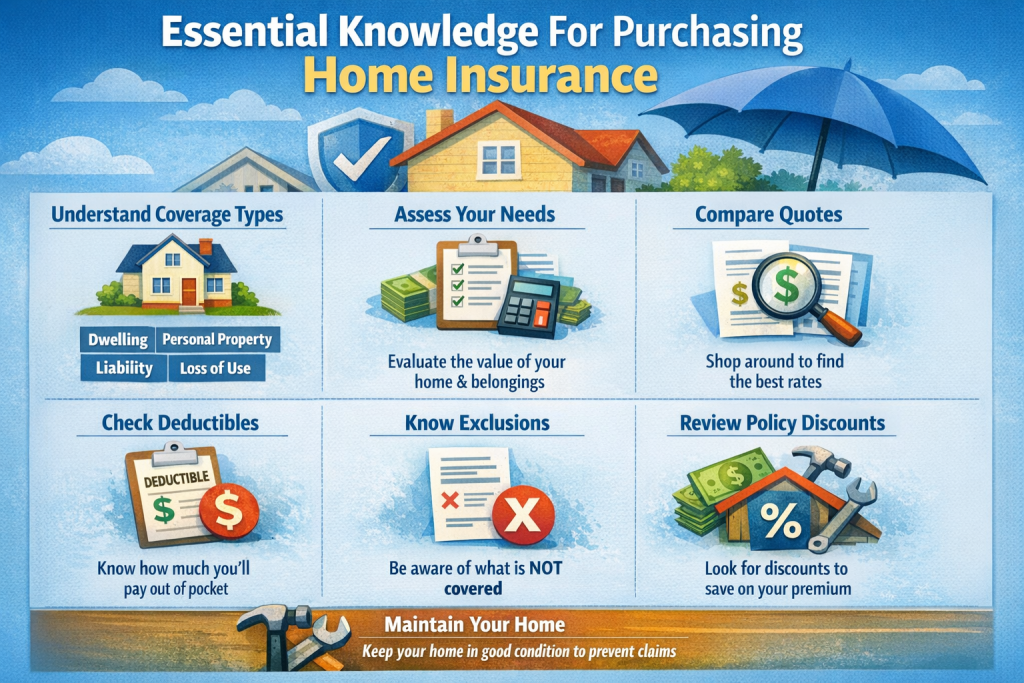

Homeowners insurance offers financial protection if your home or belongings are damaged or stolen. Most policies also include liability coverage, which protects you if someone gets hurt on your property. Insurance companies typically require you to pay a monthly or annual premium in exchange forcoverage. In case of a covered loss, you file a claim and receive payment to repair or replace damaged property. Familiarizing yourself with these concepts helps you make informed choices.

There are several key terms you will encounter when shopping for insurance. Premium is the amount you pay regularly to keep your policy active. Deductible refers to the amount you must pay out-of-pocket before your insurance kicks in. Coverage limit is the maximum amount your insurer will pay for a covered loss. Understanding these terms ensures you can compare policies accurately and avoid surprises later.

Standard home insurance policies usually cover your home, structures on your property, personal belongings, and liability. However, coverage can vary by insurer and state. Carefully review your policy and ask questions about anything you do not understand to avoid confusion. Knowing what is included in your policy gives you confidence when unexpected events occur. Assessing Your Home's Unique Coverage Needs

Every home is different, so your insurance needs may not match your neighbor's. The location of your home plays a significant role in the type of coverage you need. Homes in areas prone to natural disasters, such as floods or earthquakes, may require additional coverage. Considering your house's age, size, and features helps you determine the appropriate level of protection. Addressing these factors ensures you are not underinsured. Also, understanding the Basics of homeowners' insurance is essential.

Next, think about your lifestyle and personal situation. For example, families with children or pets may need higher liability coverage. If you own valuable items such as jewelry or art, you may want additional protection for those items. Evaluating your specific risks allows you to choose a policy that fits your life, rather than a one-size-fits-all option.

Many homeowners overlook the importance of future upgrades or renovations. Planning for improvements can affect your coverage needs. If you are considering a remodel or adding a pool, you should inform your insurer. Regularly reassessing your policy helps you maintain the right level of coverage as your needs change. Comparing Different Types of Insurance Policies

While shopping for home insurance, you will find several policy types, often known as "forms." The most common is HO-3, which covers most risks for the structure and personal property, except those specifically excluded. Another popular option, HO-5, offers broader coverage and typically provides higher limits for personal belongings. HO-1 and HO-2 policies are more basic and may only cover specific perils, making them less comprehensive.

It is important to review the fine print for each policy type carefully. Some forms provide coverage for additional living expenses if your home becomes uninhabitable, while others do not. Taking the time to understand what each form covers and what it does not helps you avoid costly gaps in protection. Comparing policies from several providers can also reveal better deals or features.

Each homeowner's situation may fit one type of policy better than another. For example, owners of older homes may need a specific policy designed for historic properties. Condo owners and renters also have specialized policy forms. Researching your options gives you more confidence when choosing the best policy for your needs.

Evaluating Coverage Limits and Deductibles And Understanding the Basics of Homeowners Insurance

Carefully choosing your coverage limits is crucial for adequate protection. The limit should reflect the cost to rebuild your home, not just its market value. Many people underestimate this amount, putting themselves at risk of paying out of pocket after a disaster. Additionally, your policy should cover the full replacement cost of your belongings whenever possible.

Deductibles play a big role in determining your insurance costs. A higher deductible usually means lower premiums, but you will pay more upfront when making a claim. Conversely, a lower deductible results in higher premiums, but less out-of-pocket expense if disaster strikes. Weighing these trade-offs helps you balance affordability and peace of mind.

Reviewing your limits and deductibles every year is a smart move. As the value of your home or possessions changes, your coverage should keep up. If you make major purchases or home improvements, adjusting your credit limits helps ensure you stay fully protected. Regular check-ins with your insurer can help you avoid unpleasant surprises after a loss. Identifying Essential Add-Ons and Exclusions

Standard home insurance policies do not cover every risk. Common exclusions include floods, earthquakes, and certain types of water damage. If you live in a high-risk area, you may need to purchase separate policies for these perils. Failing to recognize exclusions can lead to significant financial losses.

Optional add-ons, also called endorsements or riders, can fill important coverage gaps. For example, you might add coverage for sewer backups, identity theft, or expensive personal items. Evaluating your risks and discussing available add-ons with your insurance agent can enhance your protection. Choosing the right endorsements will help you avoid surprises from hazards unique to your home or lifestyle.

Reading the list of exclusions in your policy is just as vital as understanding what is included. If anything seems unclear or concerning, do not hesitate to ask your insurer for clarification. Understanding both add-ons and exclusions ensures your coverage matches your needs as closely as possible. Considering the Value of Personal Property Coverage

Personal property protection is a key component of any homeowners' insurance policy. This part of your policy covers loss or damage to your belongings, including furniture, electronics, and clothing. Typically, insurers offer either actual cash value or replacement cost coverage for personal property. Actual cash value accounts for depreciation, while replacement cost provides funds to purchase new items.

Inventorying your possessions helps you determine if your coverage is sufficient. Listing items room by room, along with photos and receipts, provides a clear record in case you ever need to file a claim. Reviewing the total value of your belongings may reveal that you need higher coverage limits, especially if you own high-end or specialty items.

Certain valuable items, such as jewelry, collectibles, or musical instruments, may be subject to sub-limits under a standard policy. Purchasing scheduled personal property coverage can ensure these items are fully protected. Regularly updating your inventory and your coverage prevents unfortunate surprises after a loss. Navigating the Claims Process with Confidence

Filing an insurance claim can feel stressful, especially after a disaster. Understanding the steps in the claims process in advance makes the process much easier. After a loss, you should notify your insurance company as soon as possible. Providing complete documentation, such as photos and receipts, strengthens your claim and speeds up the process.

Your insurer will typically send an adjuster to assess the damage. Being present during the inspection ensures you can point out all affected areas. Keeping clear records of your communications with your insurer helps prevent misunderstandings. Regularly following up on your claim status keeps the process moving forward.

Sometimes, claims get delayed or disputed. Knowing your rights as a policyholder can help you advocate for fair treatment. Do not hesitate to ask questions or request a review if you feel your claim was unfairly denied. Feeling confident in your knowledge helps you get the most from your insurance when you need it most. Final Tips for Choosing the Right Insurance Policy

Before you make a final decision, review your policy options carefully. Comparing quotes from several providers helps you find the best deal. Always check the financial strength and customer service ratings of any company you consider. Choosing a reliable insurer makes a big difference if you ever need to file a claim.

Consider working with a licensed insurance agent or broker. These professionals can explain your options and help tailor a policy to fit your specific needs. Asking friends or neighbors for recommendations often leads to better service and local expertise. Remember, the lowest price is not always the best value, so weigh coverage quality against cost.

Finally, review your policy details every year or after any major life change. Updating your coverage as your circumstances evolve keeps your protection current. Maintaining an open line of communication with your insurer provides peace of mind in any situation. An informed homeowner is always better prepared for the unexpected. Understanding the Basics of Homeowners Insurance is essential.

Conclusion

Purchasing home insurance is an essential step for every homeowner, offering security and peace of mind in uncertain times. By understanding the basic terms and coverage options, you can make decisions that truly protect your investment. Assessing your unique needs and comparing different policy types helps you find tailored protection, not just a generic solution. Evaluating limits, deductibles, and the importance of add-ons ensures you avoid unpleasant surprises after a loss. Personal property coverage is essential, so taking the time to inventory your belongings and review coverage gaps helps protect your valuables. Navigating the claims process with knowledge and confidence means you will be ready if disaster strikes.