Understanding types of home insurance in Florida is essential for homeowners. The unique climate and geography of the state create specific challenges. Floods, hurricanes, and other natural disasters can cause significant damage. Therefore, knowing the types of home insurance available is crucial. This article will explore various home insurance options available in Florida.

Exploring the Varieties of Home Insurance in Florida

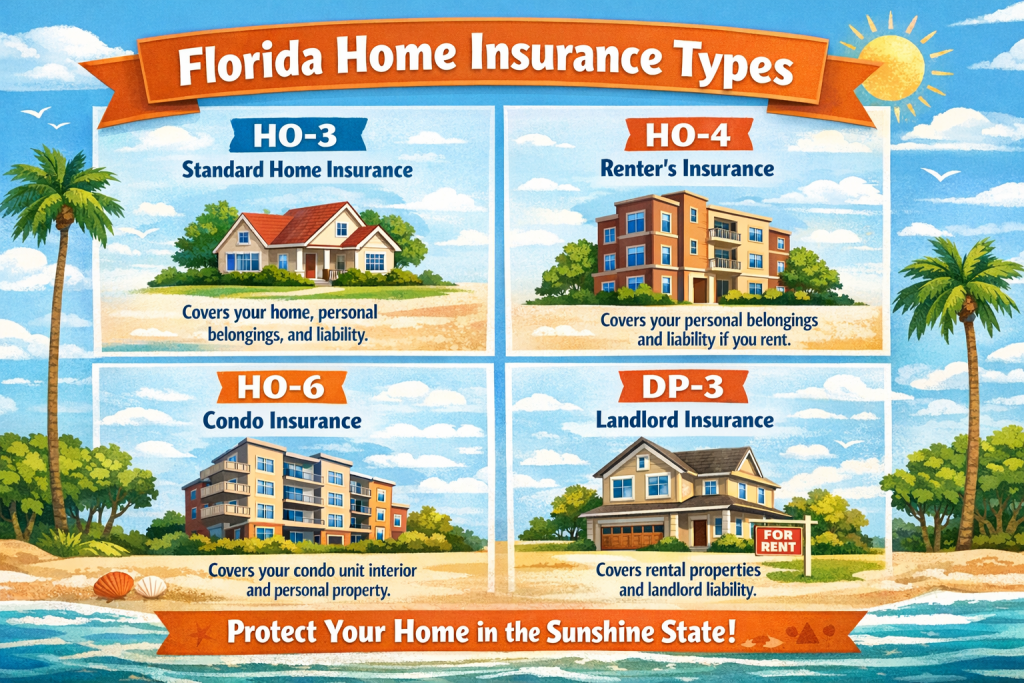

Florida homeowners can choose from several types of insurance policies. A common option is the HO-3 policy, which covers a wide range of perils. It typically protects against damage caused by fire, theft, and vandalism. Additionally, it offers liability coverage, which is vital for protecting homeowners from lawsuits. Many find this policy to be a comprehensive choice for standard homes.

Another popular option in Florida is the HO-6 policy, primarily designed for condominiums. Unlike the HO-3, this policy focuses on covering the interior of the unit. It protects personal belongings and provides liability coverage as well. Since condo associations usually cover the building structure, the HO-6 fills in the gaps. Thus, it becomes essential for condo owners to consider this type of insurance.

For homeowners living in high-risk areas, flood insurance is a must. While standard home insurance often excludes flood damage, separate flood policies are available. These policies can cover both structural and personal property damage caused by flooding. Moreover, many lenders require flood insurance for homes located in designated flood zones. Consequently, understanding this requirement can save homeowners from unexpected financial burdens.

Key Features of Florida Home Insurance Policies Explained

Several key features define Florida home insurance policies. One essential aspect is coverage limits. These limits determine how much an insurance company will pay for damages. Homeowners should evaluate their property's value and choose coverage accordingly. Having adequate limits ensures that financial protection aligns with potential repair costs. Therefore, a thorough assessment is vital for every homeowner.

Deductibles also play a significant role in insurance policies. A deductible is the amount a homeowner must pay out of pocket before the insurance kicks in. Higher deductibles often result in lower premiums, which can be appealing. However, homeowners should balance affordability with the risk of higher costs during a claim. Understanding the right deductible can significantly impact overall insurance expenses.

Another crucial feature in Florida home insurance is additional living expenses coverage. This aspect helps homeowners pay for temporary housing if a home becomes uninhabitable due to covered damages. Such coverage can prove invaluable during natural disasters, giving families some peace of mind. Additionally, many insurers offer optional coverages, like personal property replacement cost. These options allow homeowners to tailor their policies to meet specific needs.

Conclusion

In conclusion, understanding the various types of home insurance available in Florida is paramount for homeowners. From HO-3 policies for traditional homes to HO-6 policies for condos, options cater to different needs. Flood insurance remains essential for those in high-risk areas. Homeowners should carefully consider coverage limits, deductibles, and additional living expenses.